What’s happened?

One of Universal Music Group’s biggest shareholders has suddenly become a much bigger deal in the world of high finance.

Pershing Square Capital Management (PSCM), run by founder and CEO Bill Ackman, has sold a 10% stake to a group of investment firms for $1.05 billion, giving it an implied valuation of $10.5 billion.

The buyers are a consortium that includes Bermuda-headquartered insurance firm Arch Capital Group, Brazilian bank BTG Pactual, San Francisco-based ICONIQ Investment Management, and Israeli insurance firm Menora Mivtachim.

Ackman now plans to take NYC-based PSCM public sometime in the next two years, boosted by that new $10 billion-plus valuation, according to multiple reports in the financial press.

This story, of course, has a key connection to the music business.

PSCM is the exclusive investment manager for Pershing Square Holdings (PSH) – a closed-end fund that owns a significant minority stake in Universal Music Group.

According to UMG’s annual report for 2023, Pershing Square Holdings (alongside its affiliates, also managed by PSCM/Ackman) owns a 10.25% stake in Universal.

Pershing Square paid around USD $4 billion for this UMG stake (over two transactions) in 2021.

Indeed, Pershing Square is the third-largest shareholder in UMG today, behind Concerto Partners (a consortium led by Chinese tech giant Tencent, with 19.92% of UMG) and French billionaire businessman and former Vivendi president Vincent Bolloré, with an 18.01% stake.

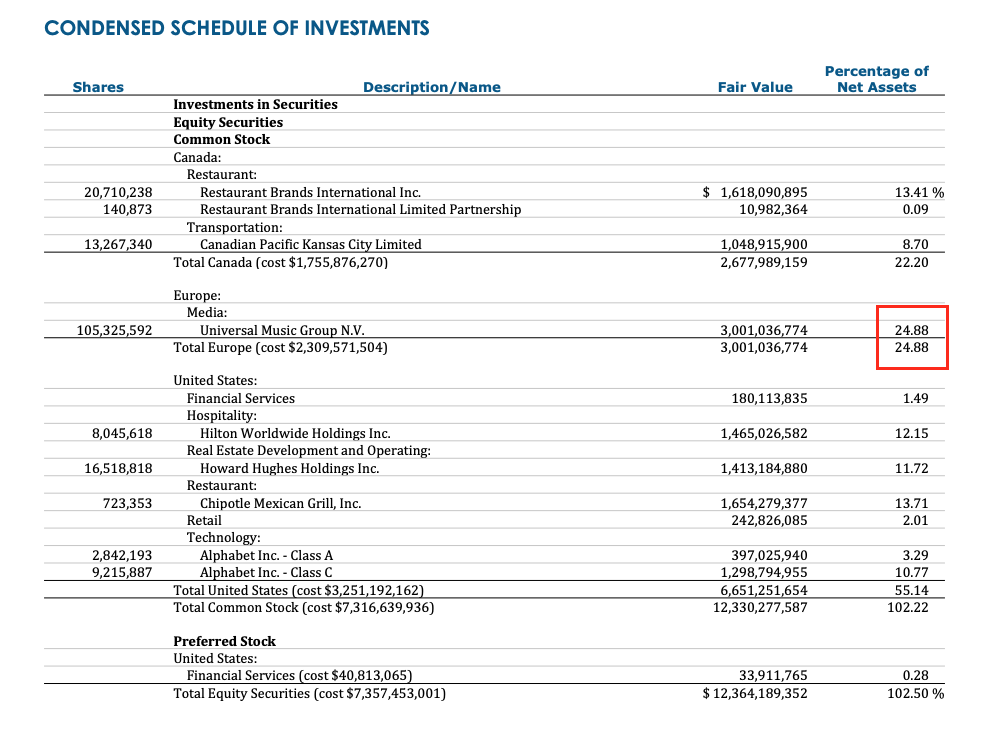

Pershing Square Holdings’ UMG stake is a crucial part of the fund’s portfolio, amounting to 24.9% of its net assets, according to PSH’s latest annual report (see below).

Ackman, who is believed to own nearly half of PSCM, has seen his own fortune rise by around $4 billion in the wake of the 10% stake sell-off, according to an estimate from the Financial Times.

How Could all of this affect UMG?

From a music industry perspective, the most interesting thing about Ackman’s 10% stake sale in his investment management firm isn’t how rich he’s gotten: it’s what he plans to do with a good chunk of the money.

According to the Wall Street Journal, around half of the $1.05 billion that Pershing Square Capital Management raised in the new stake sale will be invested in a new investment fund, Pershing Square USA.

Ackman’s ambitions for Pershing Square USA, which could launch as soon as next month, are vast: According to Bloomberg, Ackman is aiming to raise $25 billion for the new US fund.

That whopping raise could partly come from an IPO: Ackman and his team have already filed plans with the SEC to list Pershing Square USA on the New York Stock Exchange.

A prospectus filed with the SEC states that Pershing Square “believes that the [USA] Fund has the potential to be one of the largest, if not the largest, listed closed-end funds”.

PSCM will obviously be the exclusive investment manager for Pershing Square USA, just as it is for Pershing Square Holdings.

At the end of May, Pershing Square Holdings’ total Assets Under Management (AUM), including affiliates, stood at USD $19.01 billion.

So, if Ackman executes his $25 billion plan for Pershing Square USA, Pershing Square (as in, Ackman’s investment management company) could soon have some $44 billion in assets under management via closed-end funds in Europe (Pershing Square Holdings) and North America (Pershing Square USA).

And what do you think Ackman will be keen to spend his new $25 billion on?

Well, he sure loves the music business. And he sure loves Universal.

As an investor in Universal Music Group, Ackman has been a vocal advocate for the company’s strategy.

In a note to Pershing Square Holdings investors last year, he argued that UMG has been doing all the right things to capitalize on the development of AI, while working to minimize the technology’s potential to damage the music business.

“Given UMG’s continued strong market positioning and long runway for sustained earnings growth, we believe that the company’s current valuation represents a discount to its intrinsic value,” Ackman wrote.

Pershing Square’s latest annual report describes UMG as a “capital-light business that can be best thought of as a rapidly growing royalty on greater global consumption and monetization of music.”

“music is one of the lowest-cost, highest-value forms of entertainment, which is still in the early stages of monetization.”

Pershing Square’s latest annual report

The report also details Ackman’s excitement for UMG over the potential for repeated music streaming price rises in the year ahead, noting: “[M]usic is one of the lowest-cost, highest-value forms of entertainment, which is still in the early stages of monetization.”

Ackman also heaps individual praise on UMG leader Sir Lucian Grainge: Pershing Square’s annual report calls Grainge someone who “has navigated every music format and technological threat to the industry with aplomb and can only be described as an icon”.

Importantly, Ackman’s strategy, with UMG at its heart, is paying off: Pershing Square Holdings recorded 26.7% growth in NAV (Net Asset Value) in 2023.

(Alongside UMG, Pershing Square Holdings currently holds positions in Hilton Worldwide, Restaurant Brands International – owner of the Burger King, Popeyes and Tim Hortons chains – and, since 2023, Google parent Alphabet.)

So, Could Bill Ackman soon spend some of Pershing Square USA’s potential $25 billion capital on an additional stake in UMG?

Possibly, though obviously that’s just speculation.

If you follow the logic, one potential institutional seller of UMG stock is the French media empire (and former UMG owner) Vivendi, which continues to hold a 9.98% stake in UMG.

(Vivendi, remember, sold Bill Ackman the 10% of UMG that Pershing Square Holdings currently owns, agreed ahead of UMG’s Euronext listing in 2021.)

If the price is right, Vivendi’s stake in UMG (~10%) and Vincent Bolloré’s stake in UMG (~18%) might even come as a pair: via his Groupe Bolloré, Vincent Bolloré owns around 30% of Vivendi today.

But what if Ackman finds himself unable to buy a stake in UMG of sufficient size?

Perhaps he’ll look elsewhere across the music business for an opportunity — making a substantial investment in a digital service like Spotify, for instance, or a fellow music rightsholder like Warner Music Group.

Ackman has previously noted that WMG and UMG share positive trend lines for investors. In 2021, he stated, “We believe that investors have just begun to appreciate the change in industry dynamics, and as a result, have not yet given proper recognition to the value of WMG or UMG.”

However, Ackman also made clear that, in his view, UMG was the more attractive stock for Pershing Square Holdings investors.

Are there any downsides for UMG to Pershing Square’s new setup?

This story is a little knotty, but remember – if the financial press is to be believed – two new public listings are potentially coming to Pershing Square.

The first is for Pershing Square USA (PSUSA), which, as we’ve covered, could launch as early as this summer with $500 million-ish of ‘startup capital’.

That ‘startup capital’ will come from the $1.05 billion that Pershing Square Capital Management (PSCM) just raised via the sale of a 10% stake in its company, ahead of PSUSA’s planned flotation on the New York Stock Exchange.

However, PSCM itself, with a new $10.5 billion valuation in the bag, is also considering an IPO.

According to financial media reports, Ackman is considering a listing for his investment management company in the next two years, though at earliest in late 2025.

One wonders how much of his investment management company Ackman — who, remember, currently owns around half of PSCM — would be willing to sell on the stock market.

If it’s a majority-stake, or one that invites in (ironically enough) activist investors, it could spell challenges for Ackman’s headstrong investment strategy – including his seemingly unshakeable belief in the value of premium music rights.

Logically, however, it’s hard to see Ackman frittering away power at his investment management firm in such a manner.

He’ll want to maintain control, and he hardly needs the money: according to Forbes, Ackman’s personal fortune is currently worth around $9.2 billion.

A final thought…

In recent months, Bill Ackman has become a prominent political commentator on X/Twitter.

In particular, he’s been a fierce critic of what he and others say is an explosion of antisemitic sentiment in US politics since the Oct. 7 attack by Hamas on Israel, in which more than 1,100 people were killed.

An alumnus of Harvard Business School, Ackman is considered by many to have been instrumental in forcing the resignation of Claudine Gay as president of Harvard University, after she made an appearance in front of Congress last fall in which she skirted around questions on whether calling for the genocide of Jews violated Harvard’s code of conduct.

Though controversial, Ackman’s posts on X about Harvard’s president – plus his general opposition to corporate diversity, equity and inclusion (DEI) policies and his support for Israel – have caused his following on the social media platform to mushroom.

At last count, Ackman was followed by more than 1.2 million people on Elon Musk’s social media platform.

All of this might seem like risky behavior for a hedge fund manager (especially one invested in a music company that works with superstar artists who’ve shown public sympathy for Palestine).

Yet it seems that, at least to some extent, Ackman’s newly developed social media profile may actually be forming part of his business strategy.

As Reuters put it earlier this week: “The billionaire hedge fund manager has parlayed his newfound social media clout into a rich valuation for the Pershing Square Capital Management firm he started.”

It’s a similar story for Pershing Square USA (PSUSA), the new fund Ackman is trying to launch with $25 billion in the bank.

In PSUSA’s recent filing with the SEC, the soon-to-be fund pitches that it will be able to raise “significant liquidity supported by its scale, name recognition and [Ackman’s] broad following“.

It adds that it expects Ackman and Pershing Square’s “brand-name profile and broad retail following will drive substantial investor interest and liquidity in the secondary market”.

In everyday, non-finance speak, “retail following” means something much simpler: Ordinary folk.

The kind who might warm to an outspoken investment manager on social media – before throwing some of their hard-earned paycheck directly into his new fund.Music Business Worldwide

إرسال تعليق